Armed Forces

Act on Homeland Defence: New Financing Scheme for the Polish Armed Forces [ANALYSIS]

It would be possible to finance and procure new equipment for the Polish military with the use of the means contained in the annual MoD budget, long-term [multi-year] plans financed separately, BGK bonds-based Armed Forces Support Fund, or leasing, with the services rendered by the Polish and foreign businesses and agencies. These are the assumptions of the recent draft of the Act on Homeland Defence, that has recently been published.

The proposed content of the Act on Homeland Defence announced by Deputy PM Jarosław Kaczyński and Minister of Defence Mariusz Błaszczak was published on 12th November 2021 via the webpage of the Governmental Center for Legislation. Simultaneously, it was directed for inter-ministerial consultation. The organs listed in the introductory document need to make a statement on the content by 23rd November 2021. The lack of any objections shall be viewed as acceptance of the content. The draft follows the basic assumptions adopted for the Act, as showcased during the press conference that took place on 26th October 2021.

The act relevantly changes the sources, amounts, and principles involved in the defence financing scheme. Once it becomes valid on 1st July 2022, several current regulations would no longer remain in force, including the 25th May 2001 Act on Reconstruction, and Technical Modernization, and Financing of the Polish Armed Forces.

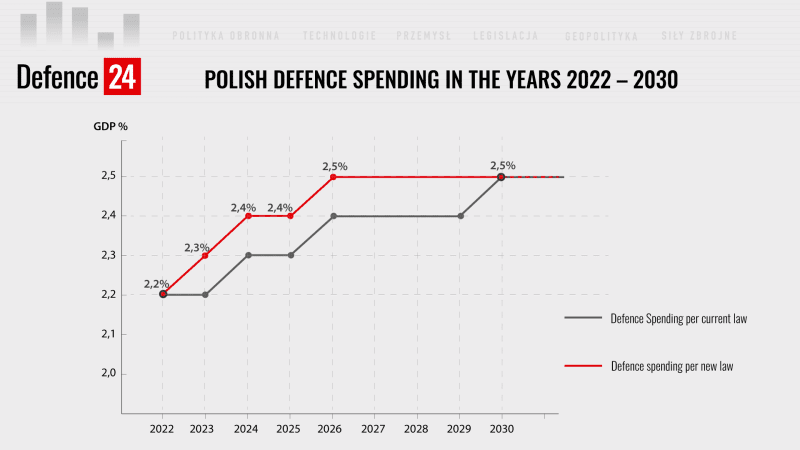

The new Act envisages increased financing of the Polish defence requirements. Per annum, the Polish defence expenditure is to be shaped as follows:

- throughout the year 2022 – 2.2% of GDP;

- throughout the year 2023 – 2.3% of GDP;

- throughout 2024 and 2025 – 2.4% of GDP;

- in 2026 and beyond - 2.5% of GDP.

The Act assumes that reaching the expenditure level equivalent to 2.5% of GDP would be quicker - it would happen 4 years earlier. Current assumptions are as follows:

- 2022-2023 - 2.2% of GDP;

- 2024-2025 - 2.3% of GDP;

- 2026-2029 - 2.4% of GDP;

- 2030 and beyond - 2.5% of GDP.

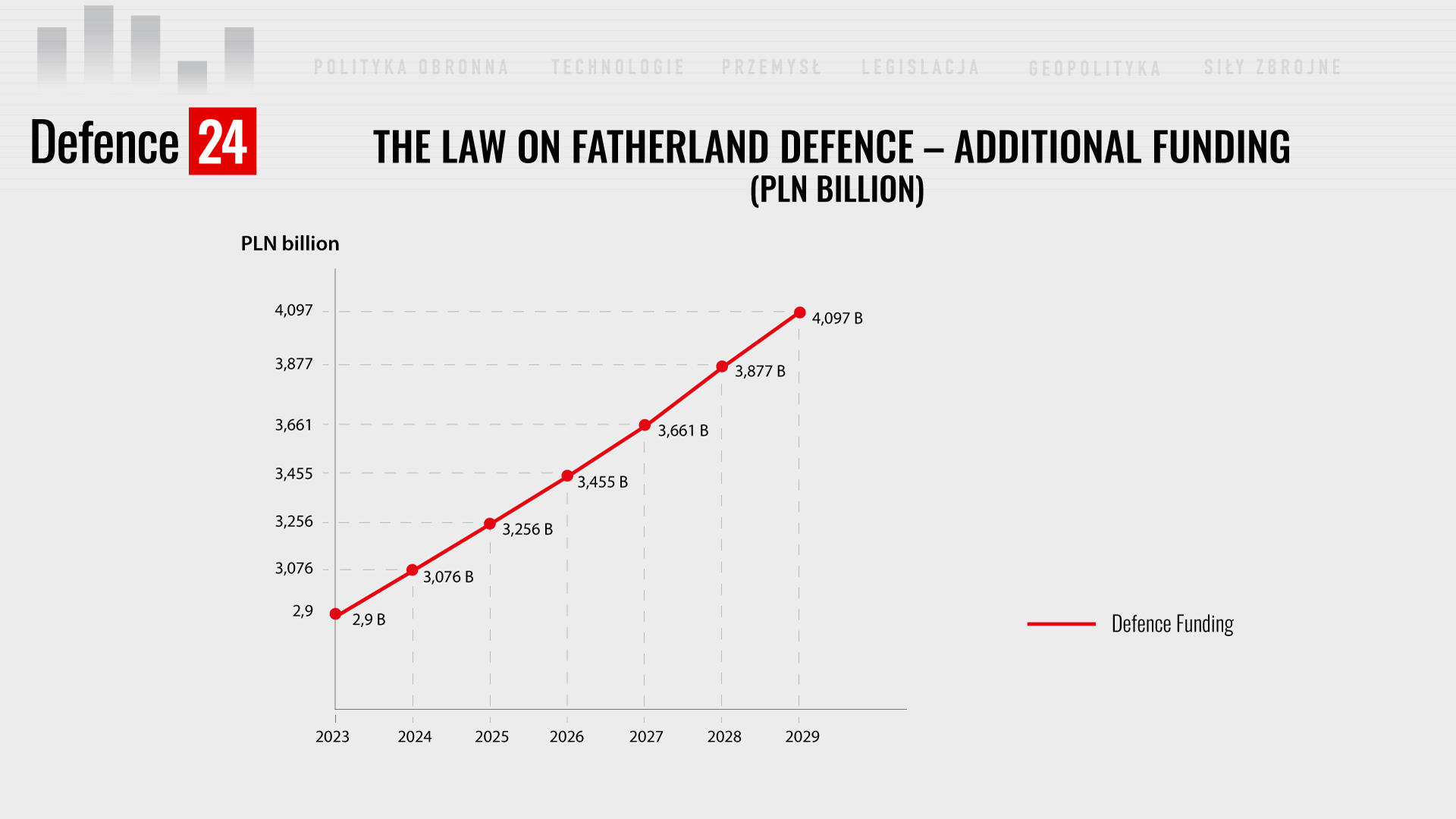

For now, it is expected that an increase of the aforesaid values characterizing the defence expenditure would translate into amounts as follows:

- in 2023 - extra PLN 2.9 billion;

- in 2024 - extra PLN 3.076 billion;

- in 2025 - extra PLN 3.256 billion;

- in 2026 - extra PLN 3.455 billion;

- in 2027 - extra PLN 3.661 billion;

- in 2028 - extra PLN 3.877 billion;

- in 2029 - extra PLN 4.097 billion;

The grand total of the acceleration of the expenditure increase to the level of 2.5% of GDP would result in the provision of extra PLN 24.321 bn. for the defence budget (according to the current expectations tied to the growth of the Polish GDP). The GDP values correspond with the year when the spending is planned.

The defence spending would consist of Part 29 of the Budget - National Defence, and spending in the national defence section in other parts of the budget. The material expenditure is to become at least 20% of the total defence spending. The Head of the Polish MoD shall take into account the Polish defence industry potential and R&D spending in the defence domain when planning the defence expenditure. The requirement to spend 2.5% on R&D would be no longer in force. The requirement in question was only complied with within the realm of the plans anyway. The R&D portion of the budget departed from the assumed 2.5%. This is the probable cause as to why this requirement has not become a part of the new Act.

The long term programmes in which the Council of Ministers designated the head of the MoD as the acting party are financed outside the GDP values defined for the given years. In practical terms, this means that the tank procurement programme initiated based on the 89/2021 resolution of the Council of Ministers issued on 9th July 2021, would increase the level of defence spending in each year during which the procurement of the M1A2 SEPv3 Abrams would be taking place.

The Council of Ministers is to define the trends and directions for the modernization of the Armed Forces every 4 years, discussing another 15-years long planning period. This would be done based on primary directions for the development of the Polish Armed Forces, as defined by the President, and based on the preparations the Polish Armed Forces are making to defend the country and meet the NATO defence planning obligations and commitments. This document would be used by the head of the MoD to develop and introduce the Armed Forces Development Programme. The programme in question defines the tasks tied to the modernization of the military, procurement of new equipment, intentions related to defence systems, commitments resulting on the grounds of international agreements or memoranda, collection and maintaining material/weapon stocks, training activities, military mobility, development of infrastructure, changing HR policy, reconversion and education.

The programme also defines the quantitative shape and composition of the individual elements of the Armed Forces. The draft Act contains no provisions on the potential increase of the number of troops to at least 250 thousand professional soldiers and 50 thousand members of the Territorial Defence Component. Realistically this number would be set by the head of the Polish Ministry of Defence, in the upcoming editions of the Armed Forces Development Programme.

According to the previous announcements, the Act would introduce relevant changes in the sources for financing of the defence expenditure. These now would include the state budget, the newly-established Armed Forces Support Fund, as well as the income gained through the sale of shares of the companies forming the industrial defence potential. The Act liquidates the current Armed Forces, Modernization Fund. The assets that would be included in the fund would become a part of the new Armed Forces Support Fund. The Fund would be established at the BGK bank. The spending within the fund would be used to fund the Armed Forces Development Programme and buyout and payment of interest tied to bonds issued by the BGK bank for the fund and cover the costs of issuing. The new fund would have numerous sources of income. The primary ones would include:

- Payments from the state budget;

- Income, from the treasury securities, mentioned in article 52 (provided by the Minister dealing with finances, on behalf of the Polish Ministry of Defence);

- Assets from the issued bonds, defined in Article 54, section 1 (as issued by the BGK bank);

- Payment, drawn from the profit gained by the National Bank of Poland;

- Funds provided via the COVID-19 prevention fund, derived from the bonds issued by BGK for the fund;

- Income resulting on the grounds support provided to foreign militaries, hosting them at the Polish training ranges, and rendering specialist military services;

- Income gained by the Military Property Agency, and funds acquired through sales of property by the said agency;

- Damages and contractual penalties, returned advance payments, guarantees, securities, and other funds received through implementation of agreements signed for the Armed Forces, and related to the procurement of military equipment, services tied to modernization, modification, or overhauls of the military equipment, scientific research and military equipment R&D, and services and construction works tied to the development of military infrastructure;

- Income gained based on payments or donations made by bodies governed by the public law, and other donations, inheritance, and transfers;

- Assets contributed by other NATO nations via reimbursement of the spending made by Poland within the framework of the NSIP programme;

- VAT refund provided to military organs, based on the implementation of tasks for the US military, resulting on the grounds of the G2G agreement between Poland and USA, on reinforced military cooperation, signed on 15th August 2020, and stemming from support provided to foreign armed forces;

- Miscellaneous income.

The establishment of the new fund at the BGK bank would create a wide array of new possibilities, but also some threats and dangers. The assets within the fund will not have to be spent during the given calendar year, and they would remain available during the upcoming years. The fund would be supported by the state, as per arrangements made by the Council of Ministers and the head of the Polish Ministry of Defence. These funds would impose a burden on the budget, but this does not apply to other, relevant fund income. The Minister of Finances may submit treasury bonds and securities into the fund, as per the request made by the Minister of Defence.

These could be issued for special financing of the defence expenditure. These securities and assets are to be bought out by the issuer in the future. It seems that direct issuing of bonds by the BGK bank would be most sufficient, as this bank would also be the "owner" of the new fund, while the bonds may be both domestic and foreign. These would be covered by a guarantee issued by the treasury, but it would be up to the bank to carry out the buyout procedure.

There are some cons of this solution as well. The bonds issued by the BGK will need to be bought back. And the funds needed to do this will need to come from the future budget, or from bonds and securities that would be issued in the upcoming years. These bonds would not be a part of the budget deficit. This would translate into an ability to create debt beyond the legally-defined deficit boundaries. Even though this may be easy and usable in the given FY - with funds becoming available - paying these back in a couple of years would increase the deficit or realistically diminish the future spending. Loans as such are useful when received, not when one needs to pay them back.

The current Armed Forces Support Fund and Armed Forces Modernization Fund operate based on an annual financial planning scheme. The plan of the current fund is an attachment of the budgetary act that is approved by the Parliament and the Senate and signed by the President. The draft version of the financial plan for the FY2022, regarding the new Fund, would be prepared by the Minister of Finances and the BGK bank. The approval is placed in the hands of the head of the Polish MoD. If the Act on Homeland Defence enters force on 1st July 2022, the plan for the new 2022 fund would only be approved in late 2022. Until then, the financial plan of the Armed Forces Modernization Plan for FY2021 would remain valid. We do not know why this concerns the year 2021, not 2022 - attachment to the FY2022 budgetary act.

The draft specifies the possibility to provide advance payments in case of military equipment, armament, or construction works/services related to construction works that have not been contracted within the public procurement scheme. After the contractor provides the securing measures arranged, the single advance payment may be as high as 33% of the arranged remuneration. Furthermore, one may provide further advance payments, provided that the contractor settles the means within the previous payments, and presents evidence that all of the previous advance payments are involved. This is a relevant solution - especially in the case of the domestic businesses who lack funds that could be used for the purpose of delivery that may be then recovered after the contract is finalized.

The ability to procure military equipment and lease it out to the Armed Forces is a new solution in the Act. This pertains to companies within the state defence industry, Industrial Development Agency, Polish Development Fund, executory agencies, and other state legal entities. Leasing instalments would be covered within the state budget, or with the use of means of the Armed Forces Support Funds. The acquisition of military equipment through leasing would also be possible in case of international agreements. Formal-legal point of view defines the leased equipment ownership to be assigned to the Armed Forces, not the lessor. This is another method of getting a modernization "loan". It would make it possible to conclude leasing agreements ad hoc, concerning new, or second-hand equipment. Poland would only be paying the leasing instalments, regularly. Concluding the leasing agreement, arrangements would be made whether the equipment can be bought at the end of the lease.

If so, then this could happen, with the equipment becoming a permanent property of the Polish Military. If this is not possible, or if Poland is not willing to use its rights, the equipment would be returned to the lessee. This solution, even though it remains convenient for the Polish Ministry of Defence, also has some cons. Leasing would make it possible to immediately acquire the armament, should it be physically available, in the event of the emergence of urgent operational requirements. During the subsequent years, the cost of instalments, maintenance and repairs would need to be covered. Planned and well thought-over procurements are a better way to go here. During recent years, a lot of unplanned procurements were justified by the urgent operational requirements, with no details disclosed to the public.

In recent years the Acts that are at the stage of inter-ministerial approval process usually pass this stage and then are approved at the Parliament and Senate, without any significant changes. This would probably be the case for the Act on Homeland Defence. One may expect some cosmetic, small amendments, and no significant changes. It seems that the Act would become valid as of July 1st 2022. It would place a mighty instrument in the hands of the Council of Ministers and the head of the Polish MoD, making it easier to rapidly modernize the Polish Armed Forces. All one needs to do is to observe, whether this Act would be put into effective use and whether it would lead to a deficit too high, that would be an excessive load imposed on the state.

Jarosław Ciślak